Overview

Government bonds are an integral part of the global financial system of any country, and India is no exception. As one of the fastest-growing economies in the world, India counts on its bond market to raise funds for its developmental and infrastructure initiatives and meet fiscal deficits. The size of the Indian bond market is fairly large with a size of $2.44 trillion; out of which $1.91 trillion is allocated to government bonds as of June 30, 2023. Thus, government bonds in India provide an avenue for governments to borrow money from varied investors, and they also serve as a secure and reliable investment option for individuals and institutions alike.

Recently, global financial services firm JP Morgan incorporated twenty-three Indian government bonds into its widely tracked emerging market (EM) debt index and the inclusion will commence on June 28, 2024. This decision will draw inflows from foreign portfolio investors and provide benefits for a couple of sectors such as banks and NBFCs. Furthermore, the increased investments will lead to lower borrowing costs for the government, underscoring the importance of government bonds in India’s financial ecosystem.

This blog will act as a beacon for understanding the different types of government bonds in India. Let’s delve into the details.

What is a Government Bond?

Government bonds, or G-Secs as they are commonly known, are debt securities that the central and state governments of India issue. These bonds are issued to raise money from the general public to cover its budgetary deficit and other infrastructure development initiatives.

A government bond in India is, in the simplest terms, a legal agreement between the issuer and the investor. The bonds have a fixed interest rate and a specified maturity date, and the investors receive regular interest payments until maturity on the face value of the bonds.

Since the issuing government backs them, government bonds are typically seen as low-risk investments. It comes in an array of tenures, ranging from a few months to several years, and offers set interest rates. Investors can purchase and sell such bonds on the secondary market since they can also be traded on stock exchanges.

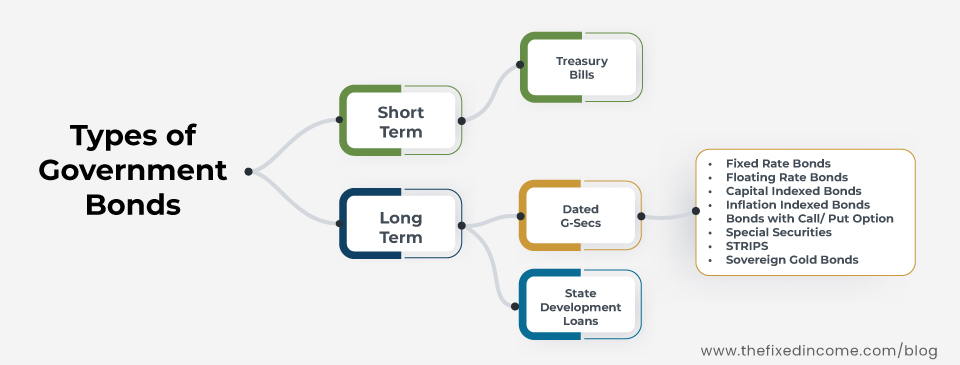

It’s important to remember that government bonds come in two varieties: short-term (also known as Treasury bills, with initial maturities of less than one year) and long-term (also known as government bonds or dated securities, with original maturities of a year or more).

What are the Types of Government Bonds?

Government bonds come in a variety of forms, each with unique benefits and features that suit various investor groups depending on their needs. The following are the variants of government bonds:

A.Treasury Bills

Treasury bills, also popularly known as T-bills, are short-term money market instruments issued by the Reserve Bank of India on behalf of the central government. T-bills are issued in three maturity periods: 91 days, 182 days, and 364 days which are issued weekly.

These securities do not have coupon payments; they are issued at a discount and redeemed at face value at the time of maturity. For example, a treasury bill that has a face value of Rs. 100 is issued at a discounted price of Rs. 98.20 which will be converted to its nominal value of Rs.100 upon redemption. If an entity buys it, the gain at redemption would be Rs. (100 minus 98.20) = Rs. 1.80.

The Reserve Bank of India auctions 91-day, 182-day, and 364-day T-bills every Wednesday

B. Cash Management Bills (CMBS)

CMBs are short-term instruments that were launched in 2010 by the Reserve Bank of India to meet temporary mismatches in cash flow. The CMBs have the same features as T-bills, but their maturity period is less than 91 days.

C. State Development Loans

State Development Loans (SDLs) are dated securities issued by state governments to fund their fiscal deficits. Interest is paid half-yearly, and the principal is repaid on the maturity date. SDLs also qualify for the State Liquidity Ratio (SLR).

D. Dated Government Securities

Dated government securities are long-term instruments of the government for mobilizing funds. They carry either a fixed or floating rate of interest, which is paid on the face value at regular intervals. Usually, the tenure of dated securities ranges from 5 to 40 years. A typical dated fixed coupon G-Sec contains the coupon, the name of the issuer, and the maturity year. For example- 7.17% GS 2028 would stand for a bond paying a coupon of 7.17% issued by the government of India and maturing in 2028.

There are various forms of dated government securities with different maturity dates.

-

Fixed Rate Bonds

These bonds have fixed coupon rates throughout their tenure and can be traded on the stock exchange. Most government bonds in India are typically issued with fixed interest rates. Since the interest rate on these bonds does not change, it provides a predictable income stream to the investors. Fixed-rate bonds are perfect for cautious investors looking for a steady source of income.

-

Floating Rate Bonds

Floating-rate bonds are debt securities with a variable coupon rate, meaning that the interest rate fluctuates based on the benchmark rate at regular intervals. Floating-rate bonds are subject to periodic changes in the rate of return. There is another type of Floating rate bond where the rate of interest is divided into two parts- a base rate and a fixed spread. This spread is decided through an auction and remains constant throughout the maturity period.

-

Capital Indexed Bonds

An index-linked bond is one in which the interest accrued on the principal amount is linked to a specific price index. In capital-indexed bonds, the principal is linked to an accepted index of inflation to protect the principal amount of the investors from inflation.

-

Inflation Indexed Bonds (IIBs)

Both coupon flows and principal amounts are protected against inflation in these bonds. The bonds are linked to an index that measures inflation, either the Wholesale Price Index (WPI) or the Consumer Price Index (CPI).

-

Bonds with a call or put option

These types of bonds have features of optionality, wherein the issuer can have the option to buy back (call option) before its final maturity or the investor can have the put option to demand repayment before maturity. Such bonds may have put, call, or both options. The transaction can only take place on the date of interest disbursal.

-

Strips

The full form of “Strips” is Separate Trading of Registered Interest and Principal of Securities. They are created by separating the cash flows associated with a regular G-Sec, which means each semi-annual coupon payment and the final principal payment to be received from the issuer, into separate securities. They are zero-coupon bonds but are made out of existing securities only and, unlike other securities, are not issued through auctions. To put it differently, a strip is a bond coupon removed from the bond so that the two components can be sold independently; one is an interest-paying coupon, and the other is a zero-coupon bond.

-

Sovereign Gold Bonds (SGBs)

Sovereign Gold Bonds are unique instruments issued by the Reserve Bank of India on behalf of the government wherein investors can invest in gold for an extended period without having to invest in physical gold. SGBs have a fixed tenure of 8 years, but an exit option is available after the 5th year. The interest earned on such bonds is exempt from capital gains tax if held until maturity.

-

Special Securities

Occasionally, the government of India, under the market borrowing program, issues special securities called oil bonds, fertilizer bonds, and food bonds to entities like oil marketing companies, fertilizer companies, and the Food Corporation of India, respectively, as compensation instead of cash subsidies.

What are the Advantages of investing in Government Bonds?

- Sovereign Guarantee– As G-secs are issued by the government, it is the liability of the government body to repay as per the stipulated terms.

- Inflation-Adjusted– The balance held in inflation-indexed bonds is adjusted against the increasing average price level. Also, the principal amount invested in capital-indexed bonds is adjusted against inflation. These are the highlighters for investors as investing in such funds increases the real value of the deposited funds.

- A Constant Source of Income– According to RBI guidelines, the interest earned on G-secs is paid every six months. Investors can earn regular income by investing in G-secs.

- Risk-free– For investors who are looking for risk-free investment, G-secs are the best option.

- Promising Long-term Returns– Returns on G-secs are similar to bank deposits but are available for a longer duration.

- Liquidity– G-secs can be bought and sold on NDS-OM (Negotiated dealing System-Order Matching). Banks and financial institutions regularly participate in this market. The securities are also tradable on stock exchanges.

- Portfolio Diversification– G-secs are useful for investors who are looking for portfolio diversification to lower the risk exposure of their portfolio.

- Can be Pledged – Gsecs can be used as cash collateral margin/ security deposit as per the SEBI margin norms.

What are the Disadvantages of investing in Government Bonds?

- Low Income– The interest earnings on these types of bonds are low due to the low risk attached to the instruments.

- Loss of Relevancy– G-sec bonds are long-term investment options that have maturity tenures ranging from 5-40 years. In due course, they can lose relevancy due to inflation, barring IIBs and capital-indexed bonds.

Why should one invest in Government Bonds?

There are multiple reasons why one should invest in government bonds. A few of them are given below:

- If an investor is looking for long-term investment, G-secs are ideal as it is available for up to 40 years of maturity.

- G-secs are the safest investments as the government issues them that is why they are also known as risk free gilt edged securities. It also provides a return in the form of interest.

- G-secs offer various investing tenures from 91 days to 40 years to meet the duration of varied liability structures of various institutions.

- G-secs can be held both in book entry and in physical form.

- G-secs can also be sold in the secondary market when needed.

- G-secs can also serve as collateral for margin requirements under equity.

- No TDS on interest income earned.

How to buy Government Bonds in India?

Here are some ways to buy government bonds in India.

- RBI Retail Direct– RBI Retail Direct helps investors invest directly in government bonds. There are benefits to investing in bonds through RBI Retail Direct, as there is no need to pay any fee for opening and maintaining the account.

- Bond platform: Investors can also buy bonds through bond platforms and start investing after completing KYC formalities. Here, investments can be started at INR 10,000. Investors can opt to invest through India’s best online SEBI-registered platform, TheFixedIncome.com, which is accessible to all. TheFixedIncome.com assists customers in making wise investments in diverse debt instruments, at the competitive prices. The information shared here on the platform is transparent and comprehensive.

- Debt Mutual Funds– Investors can also invest in debt mutual funds, which allows them to diversify their portfolios. They also have the option of accessing their money by buying and selling debt mutual funds.

- Stock Exchanges– Government bonds are listed on stock exchanges like NSE and BSE. Retail investors can participate here through their trading accounts with registered brokers.

- Others– Bonds can be invested via the buying bond ETFs which are passive investments and traded like stock ETFs on exchanges. These ETFs invest in bonds like traditional bond mutual funds and have a much lower cost than active funds.

Key Takeaways

- Safety and Creditworthiness– Government bonds are considered low-risk investments as they are issued by the government, implying a low risk of default.

- Fixed Interest Payments– Government bonds provide fixed interest payments until the bond’s maturity. The interest rate is determined at the time of issuance and remains constant throughout the bond’s duration.

- Maturity and Face Value– Government bonds have a predetermined maturity date, ranging from short-term (less than one year) to long-term (up to 40 years).

- Liquidity and Tradability– Government bonds can be bought or sold on the secondary market.

- Diversification and Portfolio Allocation– Government bonds are a great way for portfolio diversification as they provide stability, income, and diversification.

Conclusion

In summary, India’s government bond offers a wide range of bonds, ranging from security and tax savings to flexibility, to suit the different needs of investors. Investors can make informed investment decisions by aligning bond selection with their goals and risk tolerance.

Disclaimer: Investment in the securities market is subject to market risks, read all documents carefully before making any investment.

FAQs

Q1. Are all government bonds a safe investment?

Ans: Government bonds are considered low-risk investments since they are backed by the government. They offer maximum safety because the government guarantees to pay interest and repay the principal amount. As such, government bonds are generally regarded as safer investment instruments.

Q2. In what form are G-secs held?

Ans. G-secs can be held in both dematerialized and physical form. While physical bonds are held in the form of stock certificates, for G-secs to be held in Demat form, you must open a Demat account with a securities broker.

Q3. Are government bonds tax-free?

Ans. The interest income earned from government bonds is subject to taxation and is included in your annual income. The tax rate applied to this interest income is determined according to your income bracket. TDS is not applicable on interest earned.

Q4. What is the face value of a bond?

Ans. The face value represents a security’s nominal or stated value as set by its issuer. For bonds, it denotes the amount paid to the holder upon maturity, commonly known as “par value”.

Allow Retail Investors to Access Corporate Debt Markets?")