Muthoot Fincorp Limited is offering Secured, Rated, Listed, Redeemable Non-Convertible Debentures, scheduled to open on April 10, 2024, and close on April 25, 2024. This is an appealing investment prospect for investors because of its AA-/Stable rating by CRISIL Limited and backed by the company’s robust profile and impressive financial history. This blog provides insights about the company, explores the issue, and evaluates its financial performance. Below are the details of the issue:

Issue Highlights

| Issuer Name | Muthoot Fincorp Limited |

| Nature of Instrument | Secured Redeemable Non-Convertible Debentures |

| Rating | CRISIL AA-/ Stable by CRISIL |

| Seniority | Senior |

| Face Value | Rs. 1,000 per NCD |

| Base Issue Size | Rs. 10,000 lakhs (Base Issue) |

| Option to retain oversubscription | up to Rs. 26,000 lakhs (Tranche IV Issue) |

| Coupon | Up to 10.00% |

| Tenor | 26/38/60/72/94 months |

| Issue Date | April 10, 2024, to April 25, 2024 |

| Minimum Investment | Rs. 10,000 only |

Specific Terms of the NCD Public Issue across different series

Company Profile

- Muthoot Fincorp Limited is a systemically important non-deposit-taking NBFC that has been in business for over 25 years. It is a part of the “Muthoot Pappachan Group” having diverse business ventures including hospitality, financial services, inflight catering, information technology infrastructure, automobile sales and services, and real estate.

- Within the Indian market, Muthoot Fincorp Limited is a prominent gold loan player. As of December 31, 2023, the Gold loan portfolio of the company comprised approximately 31.38 lakh loan accounts.

- Besides gold loans, Muthoot Fincorp Ltd. also offers foreign exchange conversion and money transfer services as sub-agents for several registered money transfer agencies. Moreover, it is also involved in the following ventures:

- Generating and selling wind energy through its wind farms situated in Tamil Nadu.

- Engaging in real estate activities by partnering with joint venture developers to develop land parcels owned by the company.

- Muthoot Fincorp Limited operates in 3,683 branches located across 24 states, including the union territory of Andaman & Nicobar Islands and Delhi, and employs 20,645 employees.

Key Operational and Financial Parameters (Standalone)

(Rs. in lakhs)

| Particulars | As of Dec. 31st. 2023 | FY 2023 | FY 2022 | FY 2021 |

| AUM | 20,48,733.37 | 17,61,507.49 | 17,32,313 | 18,68,938 |

| Profit after tax for the year | 32,302.15 | 45,981.08 | 34,685.13 | 36,953.74 |

| Net worth | 4,36,121.45 | 3,89,303.45 | 3,44,949.33 | 3,20,078.80 |

| Interest Income | 2,64,860.50 | 3,32,167.53 | 3,18,760.74 | 2,98,476.23 |

| % Net Stage 3 Loans on Loans | 3.20% | 0.58% | 1.57% | 1.01% |

| Tier I Capital Adequacy Ratio (%) | 15.72% | 16.48% | 14.73% | 12.09% |

| Tier II Capital Adequacy Ratio (%) | 4.58% | 4.86% | 4.69% | 4.76% |

Financial Metrics across Muthoot Fincorp Limited’s Businesses.

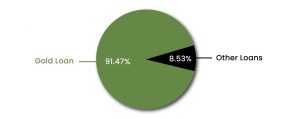

- As of December 31, 2023, MFL had approximately 31.38 lakh Gold loan accounts, aggregating to 18,73,876.00 Lakhs, which comprised 91.47 % of its total loan portfolio.

- For nine months period ended December 31, 2023, and Fiscal 2023, Fiscal 2022 and Fiscal 2021 revenues from their Gold loan business constituted 87.77%, 92.09%, 93.04%, and 93.60% of MFL’s total income on a standalone basis as per Ind AS, respectively.

- For the nine months ended December 31, 2023, Fiscal 2023, Fiscal 2022, and Fiscal 2021, MFL’s Gold loan portfolio yield (representing interest income on gold loans as a percentage of average outstanding Gold loans), were 18.57%, 20.12%, 18.74% and 21.62% per annum, respectively, on a standalone basis as per Ind AS.

- As of December 31, 2023, March 31, 2023, March 31, 2022, and March 31, 2021, the Company held 47.86 tonnes, 48.01 tonnes, 54.03 tonnes, and 59.40 tonnes, respectively, of gold jewelry, as security for all gold loans.

Competitive Strengths

- The company stands out as one of the largest Indian NBFCs primarily engaged in the gold loans portfolio, boasting extensive experience, a strong brand image, and a proven track record in gold loans throughout India.

- The company has an extensive branch network with a significant presence in Southern India.

- A proficient senior management team and a highly skilled workforce.

Rating Rationale

The rating rationale describes the following primary factors impacting the ratings of Muthoot Fincorp Limited:

Strengths

-

Backed by the extensive experience of its promoters, the company has established a strong presence in gold financing.

MFL has secured a market position in gold financing, with the promoters engaged over seven decades of experience in lending against gold jewelry. Over time, the group has built a strong reputation and brand recognition in South India and has a suitable assessment and underwriting approach. In fiscal 2023, MFL’s gold loans AUM amounted to Rs 17,942 crore.

-

Diversified product range of the MPG group

MPG has expanded its product portfolio over the past years, operating across five major segments: gold jewelry loans, two-wheeler financing, microfinance, housing finance, and small business loans. As of March 31, 2023, the managed assets under management (AUM) of MPG is around Rs 31,587 crore, compared to Rs 28,308 crore as of March 31, 2022. Despite a decrease from 64% in March 2022 to 57% in March 2023, gold loans remain the largest segment of MPG’s portfolio. CRISIL Ratings anticipates that gold loans will continue to hold the largest AUM share over the medium term.

-

Enhanced capitalization following the recent infusion.

On a standalone basis, MFL’s net worth amounted to Rs 4,050 crore (including CCCPS) as of March 31, 2023, compared to Rs 3,602 crore as of March 31, 2022. This capitalization is further supported by minimal asset-side risks, due to the security of gold jewelry, which is both liquid and in the lender’s possession.

-

Healthy asset quality in the gold loan segment to bolster the overall asset quality of the group.

As of March 31, 2023, MFL’s gross NPAs stood at 2.11%, against 2.88% as of March 31, 2022. The Reserve Bank of India’s clarification issued in November 2021 had a negligible impact on NPAs, as gold loans are demand loans with both interest and principal due at the tenor’s end. However, CRISIL Ratings notes that, due to asset quality concerns and the pandemic, the company has progressively reduced its exposure to the SME segment, and has shifted its focus to gold loan products. Additionally, the company regularly conducts auctions of gold loans which would help to keep gross NPAs below 1% in the gold loan segment.

-

Enhancing earnings outlook for gold loan business.

Over the past 2-3 years, MFL’s profitability on the standalone level has improved due to increased returns from the gold business during the pandemic, consistent reduction in overall opex, and low credit costs.

Weakness

-

Area-based concentration in the portfolio

High geographical concentration remains significant, with South India representing around 60% of the gold loan portfolio as of March 31, 2023, compared to 70% as of March 31, 2019. This reduction was attained through increased business per branch in non-southern branches, the establishment of new branches in North, East, and South India, and the closure or merger of non-viable branches in South India.

-

Potential difficulties linked with non-gold loan segments

As of March 31, 2023, non-gold segments accounted for 43% of the total portfolio. While MPG has successfully expanded these businesses and increased its segmental share over the past 2-3 years, there are potential challenges linked to the maturity of the loan portfolio and asset quality.

(Source: Rating Rationale)

Investor Categories

In a bond public issue, investor categories can be defined as the various segments or types of investors eligible to take part in the offering. The allocation ratio, guided by regulatory bodies such as SEBI, depicts how the issuer distributes the existing bonds among different investor categories. Here is the allocation ratio for the Muthoot Fincorp Limited Public Issue across these categories.

Category I- Institutional Portion- 5% of the overall issue size- Public Financial Institutions, Insurance companies, Scheduled Banks, Provident Funds, AIFs, etc.

Category II– Non-institutional Investors- 35% of the overall issue size- Companies, Co-operative Banks, Trusts, Partnership Firms, Association of Persons, etc.

Category III– Retail- 60% of the overall issue size- Resident Indian Individuals or Hindu Undivided Families through Karta applying for an amount aggregating up to and including Rs. 10,00,000.

How to Apply through TheFixedIncome.com?

Information Memorandum:

The Information Memorandum (IM) is a thorough document designed to equip investors with comprehensive details regarding the bond issue. It encompasses an extensive examination of the issuer’s business, financial background, management team, specifics of the offerings, associated investment risks, and allocation of funds from the issue. Moreover, it includes regulatory and legal disclosures to ensure transparency and compliance with regulations.

Given below is the link to the Information Memorandum of bond public issue of Muthoot Fincorp Limited:

https://www.thefixedincome.com/storage/bondprimary_imfiles/1712055544muthootfincorpIM.pdf

Conclusion

In summary, the bond public issue offered by Muthoot Fincorp Limited presents a lucrative prospect for investors keen on investing in Secured Rated Listed Redeemable Non-Convertible Debentures. This issue allows investors to potentially capitalize on the returns offered by this offering. Nonetheless, investors must read the Information Memorandum (IM) thoroughly, and evaluate their risk appetite, and investment goals before investing.

Disclaimer: This article is based on publicly available information and other sources believed to be reliable. The information provided in this article is intended for general, educational, and awareness purposes only and should not be considered a comprehensive disclosure of every material fact. It should not be interpreted as investment advice for any individual or entity. The article makes no guarantees regarding the completeness or accuracy of the information and disclaims all liabilities, losses, and damages arising from the use of this information. Investments in debt securities/ municipal debt securities/securitized debt instruments are subject to risks including delay and/ or default in payment. Read all the offer-related documents carefully

Allow Retail Investors to Access Corporate Debt Markets?")