Muthoot Finance Limited is coming up with Secured, Rated, Listed, Redeemable Non-Convertible Debentures on January 08, 2024, and closing on January 19, 2024. This is an attractive investment opportunity for investors because of its AA+/Stable rating by ICRA along with the company’s robust profile and impressive financial track record. This blog provides insights about the company, the issue, and its financial performance. Below are the details of the issue:

Issue Highlights

| Issuer Name | Muthoot Finance Limited |

| Nature of Instrument | Secured Rated Listed Redeemable Non-Convertible Debentures |

| Rating | AA+/Stable by ICRA |

| Seniority | Senior |

| Face Value | Rs. 1,000 per NCD |

| Base Issue Size | Rs. 100 crore |

| Option to retain oversubscription | Rs. 900 crore |

| Coupon | Up to 8.50% |

| Tenor | 24/36/60 months |

| Issue Date | January 08, 2024, to January 19, 2024 |

| Minimum Investment | Rs. 10,000 only |

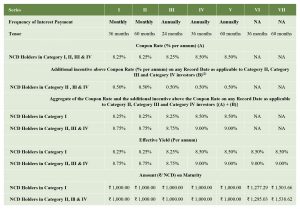

Specific Terms of the NCD Public Issue across different series

Company Profile

- Muthoot Finance Limited (MFL) holds the position of being India’s largest gold loan NBFC in terms of loan portfolio. It provides gold loans on simple terms and conditions to people from each segment of society. The gold loan range begins from ₹ 1500 and there is no maximum limit.

- Muthoot Finance Limited is an “Upper Layer NBFC” (NBFC-UL) headquartered in the south Indian state of Kerala. It has been India’s No. 1 Most Trusted Financial Services Brand 2023 for the 7th Year by TRA’s Brand Trust Report.

- The company services through 4,745 branches across 29 states/union territories in India with more than 28,000 team members.

- As of September 30, 2023, the Gold Loan portfolio stood at Rs.67,517 million comprising approximately 8.52 million loan accounts in India.

- As of September 30, 2023, the gross loan assets under management stood at Rs. 690,016 million.

- A few of the services provided by Muthoot Finance Limited include:

a) Gold loan

b) Housing finance

c) Personal loan

d) Microfinance

e) Corporate loan

f) Business loan

g) Vehicle loan

h) Mutual fund

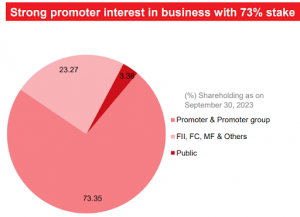

Shareholding Pattern

Performance Highlights of Muthoot Finance Limited as of September 30, 2023

Financial Parameters of the Company:

(Rs. in million)

| Particulars | FY 2021 | FY 2022 | FY 2023 |

| Net Worth | 1,52,388.93 | 1,83,445.72 | 2,10,619.28 |

| Profit after Tax | 37,221.78 | 39,543.04 | 34,753.31 |

| Interest Income | 1,03,285.29 | 1,09,560.28 | 1.03,686.11 |

| % Stage 3 Loans on Loans (Principal Amount) | 0.88% | 2.99% | 3.79% |

| % Net Stage 3 Loans on Loans (Principal Amount) | 0.77% | 2.68% | 3.40% |

| Tier 1 Capital Adequacy Ratio | 26.31% | 29.10% | 31.01% |

| Tier II Capital Adequacy Ratio | 1.08% | 0.87% | 0.76% |

Financial Metrics across Muthoot Finance Limited’s Businesses

- For the years ended March 31, 2021, 2022, and 2023 revenues from MFL gold loan business constituted 95.88%, 96.67%, and 95.10% respectively of their total income.

- Since July 2013, MFL has raised ₹ 1,96,068.51 million in non-convertible debentures issued under the public issue route. As of September 30, 2023, 0.10 million high net-worth and retail individuals had invested in their secured and unsecured debentures (subordinated debt).

- MFL’s average disbursed gold loan amount outstanding was ₹ 75,940 per loan account as of March 31, 2023. For the year ended March 31, 2023, MFL’s loan portfolio earned, on an average, interest of 1.48% per month, or 17.70% per annum.

- As of March 31, 2021, 2022, and 2023, MFL’s portfolio of the outstanding principal amount of gross Gold Loans under management was ₹ 519,265.70 million, ₹575,313.13 million, and ₹618,753.19 million respectively, and approximately 170.61 tons, 187.04 tons and 179.93 tons respectively, of gold jewelry that was held by MFL as security for Gold Loans.

- For the year ended March 31, 2021, 2022, and 2023 MFL’s total income was at ₹ 105,743.59 million, ₹ 110,983.93 million, and ₹105,437.48 million which shows a year-over-year increase of 21.23%, 4.96% and a decline of 4.99% respectively

- MFL’s loan assets portfolio has grown from ₹ 33,690.08 million as of March 31, 2009, to ₹ 632,097.68 million as of March 31, 2023.

Rating Rationale

The rating rationale outlines the following key factors influencing the ratings of Muthoot Finance Limited:

Strengths

-

Established franchise and leading market presence in the gold loan segment

MFL has been in the gold loan business for around two decades and is India’s largest gold loan-focused. As of September 30, 2023, the gold loan portfolio stood at Rs. 67,517 crores comprising approximately 8.52 million loan accounts in India serviced through 4,745 branches across 29 states/union territories.

-

Healthy earnings performance, notwithstanding moderation due to significant competitive pressure in recent quarters

MFL’s (standalone) net profitability was 5.3% in Q1 FY2024 and 4.9% in FY2023 (5.9% in FY2022). The annualized return on average net worth (standalone) was 18.5% in Q1 FY2024 and 17.6% in FY2023 (23.5% in FY2022)

-

Stable capitalization over the medium-term

MFL has a favorable capitalization profile with a standalone gearing of 2.4 times as of June 2023 and March 2023 (2.8 times as of March 2022) which is supported by strong internal capital generation. The consolidated managed gearing recorded 2.7 times as of June 2023 and 2.6 times as of March 2023 (previously 2.9 times in March 2022). As of June 2023, MFL’s standalone net worth was Rs. 21,177.1 crore, slightly up from Rs. 21,061.9 crore in March 2023. The company is well-positioned to comfortably meet the medium-term capital needs of its subsidiaries without affecting its capital structure.

Weakness

-

The performance of non-gold segments remains monitorable; a significant portion of gold loans would enhance the overall quality of the portfolio

MFL’s standalone portfolio comprises primarily of gold loans and it has expanded its exposure through its subsidiaries. At present, the consolidated loan portfolio is concentrated towards gold loans, comprising 86.0% of the loan book while microfinance, affordable housing, and vehicle finance accounted for 9.1%, 2.0%, and 0.6%, respectively, as of June 2023. The pandemic affected the performance of the non-gold segments because of the unsecured nature of the microfinance business and the average credit profile of the borrowers in the housing and vehicle finance segments. MFL’s success depends on its capacity to grow its non-gold businesses while upholding good asset quality. This is crucial over the medium to long term, considering the unsecured nature and inherent risks associated with some of these businesses compared to gold loans.

-

Operations focused in South India

MFL’s operations are largely concentrated in South India, which constituted 59% of its total branch network and 48% of its total loan portfolio as of June 2023. The share of the portfolio in South India has reduced from 57% in March 2015.

Investor Categories

The investor categories in a bond public issue are the various segments or types of investors who can participate in the offering. The allocation ratio is determined by the issuer per guidelines set by regulatory bodies such as SEBI for distributing the existing bonds among different sets of investors. Here is the allocation ratio for the Muthoot Finance Limited Public Issue across these categories.

Category I- Institutional Portion- 5% of the overall issue size- Public Financial Institutions, Insurance companies, Scheduled Banks, Provident Funds, AIFs, etc.

Category II– Non-institutional Investors- 30% of the overall issue size- Companies, Co-operative Banks, Trusts, Partnership Firms, Association of Persons, etc.

Category III– High Net-worth Individual Investors- 30% of the overall issue size- Resident Indian individuals or Hindu Undivided Families through the Karta applying for an amount aggregating to above Rs. 10,00,000 across all options of NCDs in the Issue.

Category IV– Retail- 35% of the overall issue size- Resident Indian Individuals or Hindu Undivided Families through Karta applying for an amount aggregating up to and including Rs. 10,00,000.

How to Apply through TheFixedIncome.com?

Information Memorandum:

An Information Memorandum (IM) is a comprehensive document that provides investors with in-depth information about the bond issue. It contains thorough insights into the issuer’s business, financial background, management team, details of offerings, associated investment risks, and fund allocation from the issue, besides regulatory and legal disclosures.

The link to the Information Memorandum of bond public issue of Muthoot Finance Limited is given below:

https://www.thefixedincome.com/storage/bondprimary_imfiles/1704185463MFL24.pdf

Conclusion

Summing up, the bond public issue by Muthoot Finance Limited offers an excellent opportunity for investors interested in investing in Secured Rated Listed Redeemable Non-Convertible Debentures. Investors can take advantage of this opportunity and reap the returns provided by this issue. However, before investing, investors must go through the IM thoroughly and take into account their risk appetite and investment objectives.

Disclaimer: This article is based on publicly available information and other sources believed to be reliable. The information provided in this article is intended for general, educational, and awareness purposes only and should not be considered a comprehensive disclosure of every material fact. It should not be interpreted as investment advice for any individual or entity. The article makes no guarantees regarding the completeness or accuracy of the information and disclaims all liabilities, losses, and damages arising from the use of this information. Investments in debt securities/ municipal debt securities/securitized debt instruments are subject to risks including delay and/ or default in payment. Read all the offer-related documents carefully.

2023-24: Key Points to Know")

Allow Retail Investors to Access Corporate Debt Markets?")