UGRO Capital Limited is coming up with Secured, Rated, Listed, Redeemable Non-Convertible Debentures which will be available for subscription from February 08, 2024, to February 21, 2024. This presents an attractive investment prospect for investors as it holds a credit rating of A/Stable by India Ratings. This blog will provide information about the company, its offerings, and its financial performance. The details of the issue are given below:

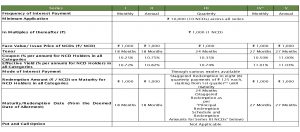

Issue Highlights

| Issuer Name | UGRO Capital Limited |

| Nature of Instrument | Secured Rated Listed Redeemable Non-Convertible Debentures |

| Rating | A/Stable by India Ratings |

| Seniority | Senior Secured |

| Face Value | Rs. 1,000 per NCD |

| Base Issue Size | Rs. 10,000 lakh |

| Option to retain oversubscription | Rs. 10,000 lakh |

| Coupon | Up to 11.00% |

| Tenor | 18/24/27 months |

| Issue Date | February 08, 2024 to February 21, 2024 |

| Minimum Investment | Rs. 10,000 only |

Specific Terms of the NCD Public Issue across different series

Company Profile

- UGRO Capital Limited is a systemically important non-deposit-taking Non-Banking Financial Company (‘NBFC’) registered with the RBI. It is a publicly listed entity on both the NSE and BSE with a market capitalization of INR 26.58 billion.

- UGRO Capital Limited is a Data Tech Lending platform that uses its strong distribution reach and Data-tech methodology to solve India’s small business credit gap.

- UGRO specializes in lending to SMEs and MSMEs, focusing on sectors like Healthcare, Education, Chemicals, Food Processing/FMCG, Hospitality, Electrical Equipment & Components, Auto Components, Light Engineering, and Micro Enterprises.

- The company’s mission is “To Solve the Unsolved”. It has a dedicated program for secured and unsecured loans aimed at MSMEs and has partnered with large OEMs to provide an end-to-end solution.

- The company caters to a varied customer base, with its branches divided into two segments. The prime branch operates in metro areas, tier 1, and tier 2 cities having customers with turnovers ranging from ₹1 crore to 15 crore, and the micro branch is located in tier 3 to 6 cities, having customers with turnovers of less than ₹1 crore.

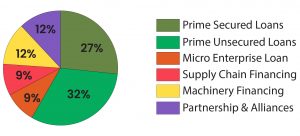

- The company offers the following loan products and solutions to MSMEs through their technology platforms:

- Prime Secured Loans

- Prime Unsecured Loans

- Micro Enterprise Loans

- Machinery Loans

- Supply Chain Finance

- Partnerships and Alliances

The product mix as of December 31, 2023, is as follows:

Top Shareholders of Equity Shares as of December 31, 2023.

| S. No. | Name of the Shareholder | Total shareholding as a % of the total number of Equity Shares |

| 1 | Danish Sustainable Development Goals Investment Fund K S | 16.46 |

| 2 | Cleasky Investment Holdings Pte Limited | 16.32 |

| 3 | NewQuest Asia Investments III Limited | 16.32 |

| 4 | Samena Fidem Holdings | 6.43 |

| 5 | Poshika Advisory Services LLP | 2.19 |

Performance Highlights of UGRO Capital Limited for the nine months ended December 31, 2023

Financial Metrics across UGRO Capital Limited’s Businesses

- UGRO’s AUM has grown from ₹ 1,31,687.51 lakh as of March 31, 2021 to ₹ 6,08,070.69 lakh as of March 31, 2023.

- As of December 31, 2023, its AUM stood at ₹ 8,36,376.40 lakh. Out of which, 53.01% of the aggregate value of AUM is secured by collaterals, 8.63% of the aggregate value of AUM is secured by receivables, 5.86% is secured by FLDG and rest 32.50% of the aggregate value of AUM is unsecured loans.

- Across the company’s offered products, as of December 31, 2023, the average ticket size stood at ₹ 16.19 lakh and the average lending rate stood at 16.3%.

- The Total Income has grown from ₹ 15,333.84 lakhs for the year ended March 31, 2021, and ₹ 31,341.59 lakh for the year ended March 31, 2022, to ₹ 68,376.28 lakh for the year ended March 31, 2023. For the nine months ended December 31, 2023, the Total Income stood at ₹ 75,129.05 lakh.

- The total borrowings as of December 31, 2023, March 31, 2023, March 31, 2022, and March 31, 2021 amounted to ₹ 4,17,292.71 lakh, ₹ 3,14,893.45 lakh, ₹ 1,80,183.86 lakh and ₹ 76,569.48 lakh respectively.

Financial Parameters of the Company:

(Rs. in lakhs)

| Particulars | FY 2021 | FY 2022 | FY 2023 |

| Total AUM | 1,31,687.51 | 2,96,980.01 | 6,08,070.69 |

| Total Income | 15,333.84 | 31,341.59 | 68,376.28 |

| Net Worth | 95,243.82 | 96,656.32 | 98,404.31 |

| Profit after Tax | 2,872.75 | 1,455.06 | 3,977.64 |

| CRAR (%) | 65.55% | 34.37% | 20.23% |

| Net Stage 3 Assets (%) | 1.75% | 1.70% | 1.31% |

Rating Rationale

India Ratings in its rating rationale outlines the following key factors influencing the ratings of UGRO Capital Limited:

Key Rating Drivers

Targeting funding to MSMEs across Diverse Regions and Sectors: UGRO is a specialized non-banking financial company primarily focused on funding Micro, Small, and Medium Enterprises (MSMEs).

Enablers in place to fuel the Growth of Franchise Networks: UGRO has invested in technology infrastructure, data analytics, human resources, as well as systems and processes, to expand its franchisee over the near-to-medium term.

Targeting for Robust Off-balance Growth: Co-lending effectiveness still to be established: UGRO is targeting to achieve significant growth in the capital-light off-balance sheet product by expanding its lending under the co-lending, direct assignment, and co-origination segments.

Adequate Capital Reserves: UGRO has built adequate capital buffers after a capital injection of INR3.4 billion during 1QFY24, leading to a higher capital base of INR13.4 billion.

Diversified Funding Mix and Lender Base: UGRO has mobilized funds from 62 financiers, which include major public sector and private sector banks.

Liquidity Status- Satisfactory: As of end-1QFY24, UGRO had a total liquidity amounting to approximately INR 5.9 billion comprising unencumbered cash, liquid investments, and unused bank lines, to meet its debt obligations for five months, excluding any inflows from collections. Additionally, UGRO maintained a surplus in one up-to-one-year on a cumulative basis at the end of FY24.

Emerging Franchise with moderate Growth; Limited Track Record, and a need for establishing Asset Quality Seasoning: UGRO started its operations in 2019 and has accumulated an AUM of INR 66.7 billion since then. Despite the robust growth in UGRO’s portfolio, the franchise size remains at a moderate level. Also, the seasoning in the portfolio is low almost 50% of the AUM generated in the 12 months ended March 2023.

Moderate Profitability: Since its inception, UGRO has maintained a moderate level of profitability, although the fiscal years 2020-2021 saw enhanced profitability due to tax write-backs.

Rating Sensitivities

Positive: A profitable and significant expansion of the franchisee ensuring asset quality, geographical diversification, and maintaining ample liquidity could lead to a positive rating action.

Negative: Funding difficulties, experiencing a decline in liquidity profile, deterioration of asset quality eroding operating buffers, and sustaining leverage exceeding 4.0x on a sustained basis will result in a negative rating action.

Investor Categories

The categories of investors in a bond public issue can be defined as the different segments or types of investors who can take part in the offering. The issuer assigns these categories based on guidelines laid by regulatory bodies such as SEBI, to allocate the available bonds among various investor groups. Here is the allocation ratio for UGRO Capital Limited’s Public Issue across these categories.

Category I- Institutional Portion- 10% of the overall issue size- Public Financial Institutions, Insurance companies, Scheduled Banks, Provident Funds, AIFs, etc.

Category II– Non-institutional Investors- 10% of the overall issue size- Companies, Co-operative Banks, Trusts, Partnership Firms, Association of Persons, etc.

Category III– High Net-worth Individual Investors- 40% of the overall issue size- Resident Indian individuals or Hindu Undivided Families through the Karta applying for an amount aggregating to above ₹ 10,00,000 across all options of NCDs in the Issue.

Category IV– Retail- 40% of the overall issue size- Resident Indian Individuals or Hindu Undivided Families through Karta applying for an amount aggregating up to and including ₹10,00,000.

How to Apply through TheFixedIncome.com?

Information Memorandum:

An Information Memorandum (IM) is an extensive document that provides investors with detailed information about the bond issue. It serves as a crucial reservoir of information for investors to thoroughly evaluate the bond and make well-informed decisions. Generally, an IM includes intricate details about the issuer’s business, financial history, management team, details of the offering, related investment risks, and allocation of funds from the issue, and also contains regulatory and legal disclosures.

The link to the Information Memorandum of bond public issue of UGRO Capital Limited is given below:

https://www.thefixedincome.com/storage/bondprimary_imfiles/1707120967UGROIM.pdf

Conclusion

Wrapping up, the bond public issue by UGRO Capital Limited presents an excellent opportunity for investors seeking to venture into Secured Rated Listed Redeemable Non-Convertible Debentures. Backed by a strong company profile, impressive financial track record, and A/ Stable ratings, these are key factors that draw investors from diverse categories. Nonetheless, investors must go through the IM thoroughly before investing and take into account their risk appetite and investment objectives.

Disclaimer: This article is based on publicly available information and other sources believed to be reliable. The information provided in this article is intended for general, educational, and awareness purposes only and should not be considered a comprehensive disclosure of every material fact. It should not be interpreted as investment advice for any individual or entity. The article makes no guarantees regarding the completeness or accuracy of the information and disclaims all liabilities, losses, and damages arising from the use of this information. Investments in debt securities/ municipal debt securities/securitized debt instruments are subject to risks including delay and/ or default in payment. Read all the offer-related documents carefully.

Allow Retail Investors to Access Corporate Debt Markets?")