In this new age, Bonds have emerged as an investment tool for people to curb their losses and earn fixed income on their investments. There are a myriad of factors that one should consider before making an investment in a bond portfolio. Investing in bonds gives you several benefits like long-term income, high degree of safety and lower risk as well as high stability — however it also comes with certain hidden risks as well that one must be aware of.

Various Bond Types & Decoding the Tax Effects

Bonds are debt instruments that represent the debt owned by the government and corporations to the investor. The entities raise funds for their various requirements like infrastructure projects, expansion, etc. Investors receive a fixed return known as coupon in exchange for investing in companies and are repaid the principal amount at maturity.

Before making an investment decision, investors should always take into consideration the return generated from the asset. But to calculate real return from an investment, it is very crucial to know the tax implications of the same.

While investing in bonds there are two types of income generated by investing in bonds: interest income, which is paid at predetermined intervals such as monthly, quarterly, semi-annually, and so on and the other is capital gain/ loss at the time of sale/ redemption of bonds.

There are different types of bonds like Government Securities, Corporate Bonds, Tax-free bonds, 54EC Bonds, Gold Bonds etc. and each has a unique structure. The two major components of investor’s return that are taxable are Interest income and capital gains. In this blog, let us try and understand the tax implications of investing in various types of Bonds.

Understanding Taxation on Interest Income and the TDS Requirements

Bonds represent a loan agreement between the lender (investor) and the borrower (government & Corporates) where the government & corporates pay regular interest on the borrowed money. The interest payments also known as coupon rates are pre-defined and specified in the offer document. Thus, when an investor invests in bonds, they will receive periodic coupon payments. Such income is taxable under the head “Income from Other Sources” as per the Income Tax Act, 1961 at the applicable slab rates.

Let’s take an example to have a more clear understanding:

Assume Mr. A invests Rs.10,00,000 in bonds that offer a 10% coupon rate payable annually. At the end of year 1, Mr. A will receive Rs.1,00,000 as interest. Suppose Mr. A’s total income is Rs. 8,00,000, which places him in the 20% tax slab as per the old tax regime. Therefore Mr. A will be liable to pay tax on Rs.1,00,000 at the rate of 20% under the “IFOS” head.

If you purchase or sell bonds in the secondary market, it is important to understand the taxation implications of accrued interest. The Interest earned on bonds bought in the secondary market is taxed on an accrual basis rather than a receipt basis.

For instance, if a bond is sold with accrued interest of Rs. 9,000 and the buyer receives Rs.12,000 in interest at the end of the year, the seller will be liable to pay tax on the accrued interest of Rs.9,000. This amount will be added to the seller’s total income rather than the buyer’s. To simplify, investors must pay taxes on the interest earned during their holding period rather than the total interest received.

Interest income earned from Bonds and Debentures is also subject to tax deduction at source. Previously, the securities held in dematerialised form and listed on recognised stock exchanges in India were exempt from TDS. However, this has been omitted in the recent Budget for FY 2023-24.

According to Section 193 of the Income Tax Act, 1961, all interest income from securities will be subject to Tax Deducted at source (TDS). Effective from April 01, 2023 TDS at the rate of 10% will be deducted from the interest income of all listed as well as unlisted Bonds. This implies that interest earned on all Bonds will now be subject to TDS.

Uncovering Capital Gain:- Tax on Bond Investments Made in the Secondary Market

When an investor sells the Bond in the secondary market, it results in a capital gain/ loss. The Capital Gain is calculated as the difference between the Sale consideration and the Cost of the asset. For instance, if an investor sells the bond in the market at a lower price than the acquisition cost, it results in a capital loss. Conversely, if the investor sells the bond at a higher price than the acquisition cost, it leads to a capital gain.

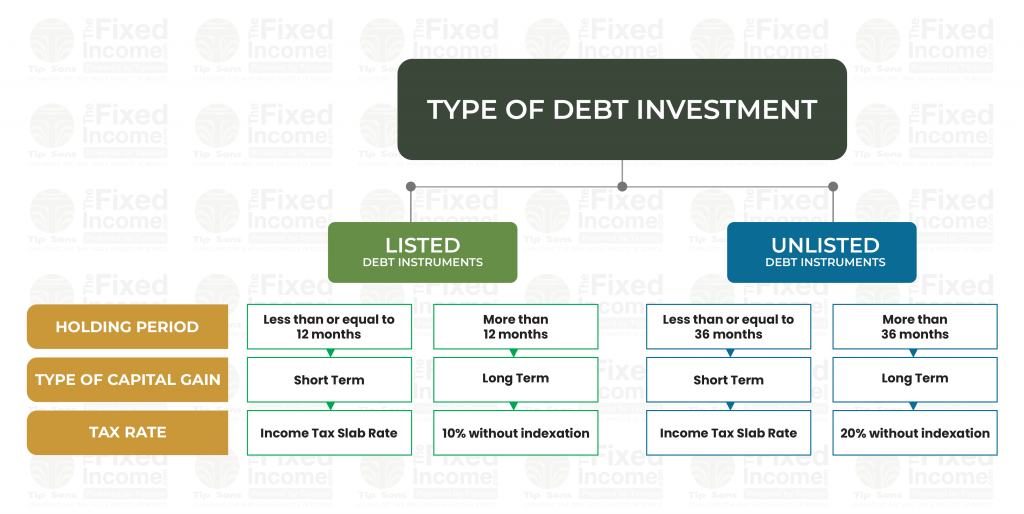

The Capital Gain tax is determined on the basis of the period of holding the bond. Period of holding refers to the time period for which the investor holds the asset i.e. duration for which the investor holds the bonds. In the case of listed bonds i.e bonds that are listed on a recognized stock exchange, if the period of holding is equal to or less than 12 months then the investor will be subject to short-term capital gains tax on the profits at their respective slab rates. If the holding period exceeds 12 months then it will be classified as long-term capital gains tax, which would be levied at a rate of 10% without indexation.

If the bonds are unlisted, meaning they are not listed on recognized stock exchanges, short term gain tax will apply if the period of holding is less than or equal to 36 months. These gains will be taxed at an individual slab rate. However, if the holding period is more than 36 months, long term capital gain tax will be applicable and it would be taxed at 20% without indexation under the Long Term Capital Gain head. The following table provides a clear understanding of taxation:

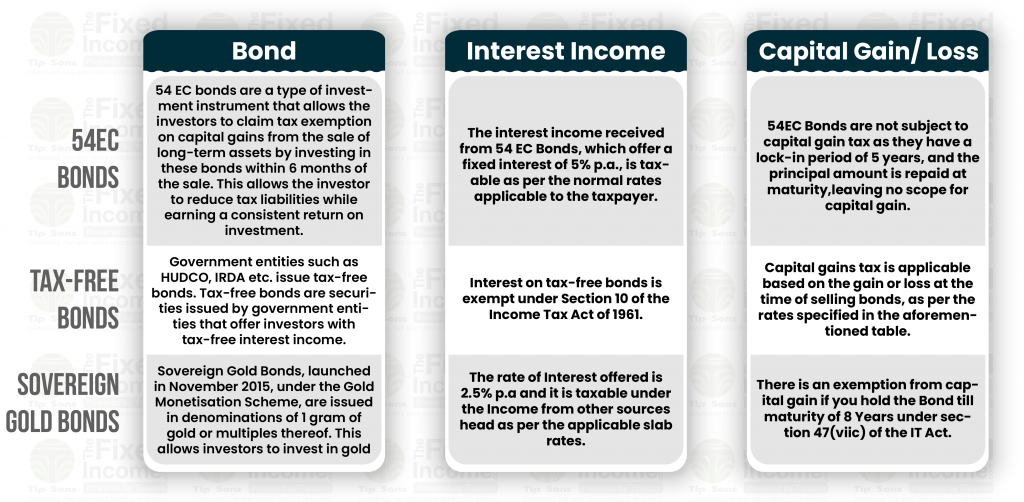

However, it is pertinent to note that the Capital indexed bonds and Sovereign Gold bonds qualify for the indexation benefits. The tax rates mentioned above apply to all regular bonds but certain bonds have unique tax treatment. The same is highlighted in the table below:

The taxation of bonds in India comes with a variety of tax implications that are dependent on the type of bond and the holding period of the investment. While bonds can be an excellent part of your portfolio, it is crucial to be aware of the various tax implications that apply to different types of fixed-income instruments. This understanding can assist you in making an informed investment decision that aligns with your specific requirements. However, given the constantly evolving and complex nature of taxation, it’s advisable to seek guidance from your tax consultant or chartered accountant to ensure an accurate estimation of your taxes.

Allow Retail Investors to Access Corporate Debt Markets?")