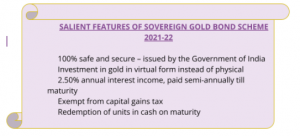

SOVEREIGN GOLD BOND SCHEME (SGB) 2021-22

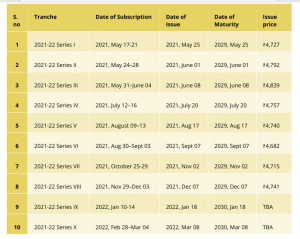

RBI announced the Sovereign Gold Bond Scheme (SGB) 2021-2022, issued in 10 tranches: six tranches in the first release, followed by four tranches.

Note, ₹50 per gram discount on the issue price is applicable for online applications. Issue price stated in the table above is after the discount. RBI will release the issue price of the upcoming tranches a few days ahead of the subscription date for each tranche.

WHAT ARE SOVEREIGN GOLD BONDS (SGBS)?

Sovereign Gold Bonds (SGBs) are a government debt security (G-Sec), issued in units of grams of gold

WHO IS THE ISSUER OF THE SGBS?

The Reserve Bank of India (RBI) issues SGBs on behalf of the Government of India.

WHY ARE SGBS ISSUED?

To finance the fiscal deficit, Government of India issues government securities (G-Sec), and SGBs are one of those securities

WHY INVEST IN SGBS AS OPPOSED TO PHYSICAL GOLD?

Risk: Mitigate the risk of holding gold in physical form

Making charges: No need to fret over incremental costs of making charges or deduction of the same when selling gold (jewellery for e.g.)

Purity: Do away with the concerns regarding the purity of gold. SGBs are linked to the price of gold of 999 purity (24 carat)

Taxation: SGBs are exempt from CGT, whereas physical gold sale attracts CGT

Interest income: Investors of SGBs earn annual interest income of 2.50%, whereas physical gold does not reap any direct interest income

ARE THERE ANY RISK ASSOCIATED WITH INVESTING IN SGBS?

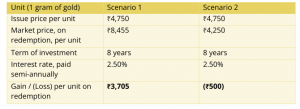

Yes, there is a risk of a capital loss should the market price of gold decline at the time of redemption

Example 1: let’s take an example of investment in 1 gram of gold today with an issue price of ₹4,750. At the time of redemption, say in 8 years from now, there could be 2 scenarios (presented in the table below):

- Scenario 1: market price of gold could be higher than the issue price, resulting in a capital gain (exempt from CGT)

- Scenario 2: market price of gold could be less than the issue price, resulting in a loss

WHERE TO BUY SGBS FROM?

Reach out to your trusted partners at https://www.thefixedincome.com/, an authorized agency, to invest in SGBs

SGBs are being sold through offices or branches of Nationalised Banks, Scheduled Private Banks, Scheduled Foreign Banks, designated Post Offices, Stock Holding Corporation of India Ltd. (SHCIL) and the authorised stock exchanges either directly or through their agents

Authorised agencies will also be providing services including change of address, early redemption, nomination, grievance redressal, transfer applications etc.

WHO IS ELIGIBLE TO INVEST IN SGBS?

Individuals. A ‘minor’ is eligible to invest, however the application has to be submitted by his/her guardian

- HUF

- Trust

- Universities

- Charitable organizations

WHAT IS THE INVESTMENT CEILING ON SGBS?

Minimum Investment: 1 gram of gold

Maximum Investment: subject to investor type (in a fiscal year)

- Individual: 4 Kg of gold. An eligible individual can invest in SGBs in his/her own name, implying each eligible family member can invest in SGBs in his/her own name

- HUF: 4 Kg of gold

- Others (Trust, Universities, Charitable Organizations): 20 Kg of gold Investment ceiling stated above is per fiscal year (April to March), and includes bonds issued under the 6 tranches, plus any purchase from the secondary market. Note, in cases of joint holding, the investment cap is applicable to the 1st applicant WHAT IS THE TERM OF INVESTMENT IN SGBS?A fixed term of 8 years. However, investors will have an option to exit after the 5th year WHAT INTEREST RATE SGBS WILL PAY TO AN INVESTOR?Fixed interest income at the rate of 2.50% per annum on the initial investment, payable semi-annually WHAT ARE THE TAX IMPLICATIONS OF INVESTING IN SGBS?Interest income: Taxable but TDS not applicableCapital gains: An individual is exempt from any capital gains tax, if held till maturity. If SGBs are transferred to an eligible investor, then indexation benefit is provided to that individual for long-term capital gains calculation

WHAT ARE THE PAYMENT OPTIONS FOR INVESTING IN SGBS?

- Cash, up to ₹20,000

- Demand draft

- Cheques

- Electronic fund transfer

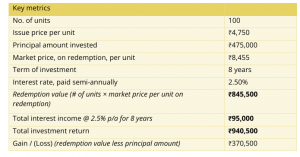

WHAT WILL BE THE RETURN ON THE REDEMPTION OF SGBS?

Cash: cash in INR equivalent to the market price of the number of units (grams) held will be credited to an investors bank account on maturity/redemption of units

Periodical interest income paid semi-annually over the term of the investment at 2.50% of the initial principal amount

Example 2: let’s consider an investment in 100 grams of gold today with an issue price of ₹4,750. At the time of redemption, say in 8 years from now, the market price of gold is ₹8,455

ARE SGBS PREMATURELY REDEEMABLE?

Yes, only after 5 years from the date of issue of that SGB tranche; redemption can be made on the next coupon payment date that will fall after 5 years from the date of issue

For premature redemption, reach out to an authorized dealer 30 days before the coupon payment date

ARE SGBS TRADABLE AND TRANSFERABLE?

Yes, on secondary securities market

Transferable to any eligible investor

CAN AN INVESTOR USE SGBS AS A COLLATERAL?

Yes, SGBs can be used as collateral for loans from banks, financial institutions, and Non-Banking Financial Companies (NBFC)

IS NOMINATION FACILITY AVAILABLE FOR SGBS?

An investor can appoint a nominee, as per the provisions of the Government Securities Act 2006 and Government Securities Regulations, 2007

CAN AN INVESTOR HOLD SGBS IN A DEMAT ACCOUNT

Can be held in a demat account

Need to specify while filling the application form

WHAT KYC DOCUMENTS ARE REQUIRED?

Aadhaar or PAN, and voter ID

GROWTH OF SOVEREIGN GOLD BONDS OVER THE PAST 6 YEARS

Sovereign Gold Bonds have witnessed a dramatic growth since their first launch in 2015. Table below summarises few key aspects, comparing the terms of Sovereign Gold Bonds issued in 2015, and now in 2021:

EARLY REDEMPTION OF SOVEREIGN GOLD BOND SCHEME 2015-16, TRANCHE 2

On 5th Feb 2021, RBI had announced the redemption price of ₹4,786 per unit of gold for the early redemption of bonds due on 8th Feb 2021 and issued under Sovereign Gold Bond Scheme 2015-16 on 8th Feb 2016

Investment return on this scheme can be calculated as below (calculated on 1 unit of investment):

- Redemption value: ₹4,786 per unit

- Total interest income: ₹369.05, @ 2.75% per annum for 5 years

- Total return: ₹5,155.05 (redemption value of ₹4,786 plus total interest income of ₹369.05). An individual investor will make a capital gain of ₹2,102 per unit (redemption value of ₹4,786 less principal amount of ₹2,684)

2023-24: Key Points to Know")

Allow Retail Investors to Access Corporate Debt Markets?")